Suppose that a scalar

}")

")

In this article, we will study the estimation and hypothesis testing of

1. The Algebra of Linear Regression

Given a sample of T values of

^2 \ \ \ \ \ (2)")

The OLS estimate of

^{\!-1} \!\!\cdot\, \frac{1}{T}\sum_{t=1}^n x_ty_t. \ \ \ \ \ (3)")

The model is written in matrix notation as:

")

")

where

Thus,

^{-1}X^Ty. \ \ \ \ \ (6)")

Similarly,

![\displaystyle \hat u = y - Xb = y - X(X^TX)^{-1}X^Ty = [I_T - X(X^TX)^{-1}X^T]y = M_Xy. \ \ \ \ \ (7)](http://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Chat+u+%3D+y+-+Xb+%3D+y+-+X%28X%5ETX%29%5E%7B-1%7DX%5ETy+%3D+%5BI_T+-+X%28X%5ETX%29%5E%7B-1%7DX%5ET%5Dy+%3D+M_Xy.+%5C+%5C+%5C+%5C+%5C+%287%29&bg=ffffff&fg=000000&s=0 "\displaystyle \hat u = y - Xb = y - X(X^TX)^{-1}X^Ty = [I_T - X(X^TX)^{-1}X^T]y = M_Xy. \ \ \ \ \ (7)")

where

![\displaystyle M_X = [I_T - X(X^TX)^{-1}X^T]. \ \ \ \ \ (8)](http://s0.wp.com/latex.php?latex=%5Cdisplaystyle+M_X+%3D+%5BI_T+-+X%28X%5ETX%29%5E%7B-1%7DX%5ET%5D.+%5C+%5C+%5C+%5C+%5C+%288%29&bg=ffffff&fg=000000&s=0 "\displaystyle M_X = [I_T - X(X^TX)^{-1}X^T]. \ \ \ \ \ (8)")

")

")

Since

")

Thus, we can verify that the sample residuals are orthogonal to

")

The sample residual is constructed from the sample estimate of

")

")

![\displaystyle \hat u = y - Xb = [I_T - X(X^TX)^{-1}X^T]y = M_Xy = M_XX b + u. \ \ \ \ \ (15)](http://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Chat+u+%3D+y+-+Xb+%3D+%5BI_T+-+X%28X%5ETX%29%5E%7B-1%7DX%5ET%5Dy+%3D+M_Xy+%3D+M_XX+b+%2B+u.+%5C+%5C+%5C+%5C+%5C+%2815%29&bg=ffffff&fg=000000&s=0 "\displaystyle \hat u = y - Xb = [I_T - X(X^TX)^{-1}X^T]y = M_Xy = M_XX b + u. \ \ \ \ \ (15)")

^{-1}X^Ty = (X^TX)^{-1}X^T(X\beta + u) = \beta + (X^TX)^{-1}X^Tu. \ \ \ \ \ (16)")

The fit of OLS is described in terms of

}")

")

2. Assumptions on X and u

We shall assume that

(a) X will be deterministic

(b)

(c)

2.1. Properties of Estimated b Under Above Assumptions

Since,

^{-1}X^Ty = (X^TX)^{-1}X^T(X\beta + u) = \beta + (X^TX)^{-1}X^Tu. \ \ \ \ \ (18)")

Taking expectations of both sides, we have,

= \beta + (X^TX)^{-1}X^T\mathop{\mathbb E}(u) = \beta. \ \ \ \ \ (19)")

And the variance covariance matrix is given by,

![\displaystyle \mathop{\mathbb E}[(b - \beta)(b - \beta)^T] = \mathop{\mathbb E}[((X^TX)^{-1}X^Tu)((X^TX)^{-1}X^Tu)^T] = \sigma^2(X^TX)^{-1}. \ \ \ \ \ (20)](http://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cmathop%7B%5Cmathbb+E%7D%5B%28b+-+%5Cbeta%29%28b+-+%5Cbeta%29%5ET%5D+%3D+%5Cmathop%7B%5Cmathbb+E%7D%5B%28%28X%5ETX%29%5E%7B-1%7DX%5ETu%29%28%28X%5ETX%29%5E%7B-1%7DX%5ETu%29%5ET%5D+%3D+%5Csigma%5E2%28X%5ETX%29%5E%7B-1%7D.+%5C+%5C+%5C+%5C+%5C+%2820%29&bg=ffffff&fg=000000&s=0 "\displaystyle \mathop{\mathbb E}[(b - \beta)(b - \beta)^T] = \mathop{\mathbb E}[((X^TX)^{-1}X^Tu)((X^TX)^{-1}X^Tu)^T] = \sigma^2(X^TX)^{-1}. \ \ \ \ \ (20)")

Thus b is unbiased and is a linear function of y.

2.2. Distribution of Estimated b Under Above Assumptions

As u is Gaussian,

^{-1}X^Tu. \ \ \ \ \ (21)")

implies that b is also Gaussian.

^{-1}). \ \ \ \ \ (22)")

2.3. Properties of Estimated Sample Variance Under Above Assumptions

The OLS estimate of variance of u,

= {\hat u}^T\hat u / (T - k) = u^TM_X^TM_Xu / (T - k) = u^TM_Xu / (T - k). \ \ \ \ \ (23)")

Since

")

where

")

and

Since,

")

that is, since the two spaces that they represent are orthogonal to each other, it follows that:

")

whenever v is a column of X. Since we assume X to be of full rank, there are k such vectors and their eigenvalue is the right hand side, which is 0.

Also since

^{-1}X^T. \ \ \ \ \ (28)")

Thus, it follows that

")

whenever v is orthogonal to X. Since there are (T – k) such vectors,

Thus

")

Let

")

Then,

")

")

As these

")

Also,

= \mathop{\mathbb E}(P^Tu u^T P) = \sigma^2I_T. \ \ \ \ \ (35)")

Thus, elements of w are uncorrelated with each other, have mean 0 and variance

Since each w has expectation of

= (T - k)\sigma^2. \ \ \ \ \ (36)")

Hence,

= \sigma^2. \ \ \ \ \ (37)")

2.4. Distribution of Estimated Sample Variance Under Above Assumptions

Since

")

when u is Gaussian, w is also Gaussian.

Then,

")

implies that

}")

Thus,

. \ \ \ \ \ (40)")

Also, b and

![\displaystyle \mathop{\mathbb E}[\hat u(b - \beta)^T] = \mathop{\mathbb E}[M_Xu u^T X (X^TX)^{-1} = 0. \ \ \ \ \ (41)](http://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cmathop%7B%5Cmathbb+E%7D%5B%5Chat+u%28b+-+%5Cbeta%29%5ET%5D+%3D+%5Cmathop%7B%5Cmathbb+E%7D%5BM_Xu+u%5ET+X+%28X%5ETX%29%5E%7B-1%7D+%3D+0.+%5C+%5C+%5C+%5C+%5C+%2841%29&bg=ffffff&fg=000000&s=0 "\displaystyle \mathop{\mathbb E}[\hat u(b - \beta)^T] = \mathop{\mathbb E}[M_Xu u^T X (X^TX)^{-1} = 0. \ \ \ \ \ (41)")

Since b and

2.5. t Tests about

We wish to test the hypothesis that the ith element of

The t-statistic for testing this null hypothesis is

^2} \ \ \ \ \ (42)")

where

^{-1}}")

Under the null hypothesis,

. \ \ \ \ \ (43)")

Thus,

. \ \ \ \ \ (44)")

Thus,

} / {\sqrt{\sigma^2 \xi^{ii}}}}{\sqrt{s^2 / \sigma^2 }} \ \ \ \ \ (45)")

Thus the numerator is N(0, 1) and the denominator is the square root of a chi-square distribution with (T – k) degrees of freedom. This gives a t-distribution to the variable on the left side.

2.6. F Tests about

To generalize what we did for t tests, consider that we have a matrix

")

Since,

^{-1}). \ \ \ \ \ (47)")

Thus, under

^{-1}R^T). \ \ \ \ \ (48)")

Theorem 1 If

is a

vector with

and non singular

, then

.

Applying the above theorem to the

^T (\sigma^2R(X^TX)^{-1}R^T)^{-1}(Rb - r) \sim \chi^2 (m). \ \ \ \ \ (49)")

Now consider,

^T (s^2R(X^TX)^{-1}R^T)^{-1}(Rb - r) / m. \ \ \ \ \ (50)")

where sigma has been replaced with the sample estimate s.

Thus,

![\displaystyle F = \frac{[(Rb - r)^T (\sigma^2R(X^TX)^{-1}R^T)^{-1}(Rb - r)] / m}{[RSS / (T - k)]/ \sigma^2} \ \ \ \ \ (51)](http://s0.wp.com/latex.php?latex=%5Cdisplaystyle+F+%3D+%5Cfrac%7B%5B%28Rb+-+r%29%5ET+%28%5Csigma%5E2R%28X%5ETX%29%5E%7B-1%7DR%5ET%29%5E%7B-1%7D%28Rb+-+r%29%5D+%2F+m%7D%7B%5BRSS+%2F+%28T+-+k%29%5D%2F+%5Csigma%5E2%7D+%5C+%5C+%5C+%5C+%5C+%2851%29&bg=ffffff&fg=000000&s=0 "\displaystyle F = \frac{[(Rb - r)^T (\sigma^2R(X^TX)^{-1}R^T)^{-1}(Rb - r)] / m}{[RSS / (T - k)]/ \sigma^2} \ \ \ \ \ (51)")

In the above, the numerator is a }")

}")

Hence, the variable on the left hand side has an exact }")

is a fixed quantity, not a random variable.

is a fixed quantity, not a random variable.

.

.  . On day 3, you collect new data and construct a 95 percent confidence interval for an unrelated parameter

. On day 3, you collect new data and construct a 95 percent confidence interval for an unrelated parameter  .

.  .

.  into two disjoint sets

into two disjoint sets  and

and  and we wish to test:

and we wish to test: ")

the alternate hypothesis.

the alternate hypothesis.  be its range. Let

be its range. Let  be the rejection region.

be the rejection region. = \mathbb{P}_{\theta}(X \in R) \ \ \ \ \ (2)")

). \ \ \ \ \ (3)")

Test: A test with size less than or equal to

Test: A test with size less than or equal to  is called a simple hypothesis.

is called a simple hypothesis.  or

or  is called a composite hypothesis.

is called a composite hypothesis. ")

")

")

}") where

where  is known. We want to test

is known. We want to test  versus

versus  . Hence

. Hence ![{\Theta_0 = (- \infty, 0]}](http://s0.wp.com/latex.php?latex=%7B%5CTheta_0+%3D+%28-+%5Cinfty%2C+0%5D%7D&bg=ffffff&fg=000000&s=0 "{\Theta_0 = (- \infty, 0]}") and

and }") .

. ")

.

.  : \overline{X} > c \} \ \ \ \ \ (8)")

= \mathbb{P}_{\mu}(X \in R) \\ = \mathbb{P}_{\mu}(\overline{X} > c) \\ = \mathbb{P}_{\mu}\left( \frac{\sqrt{n}(\overline{X} - \mu)}{\sigma} > \frac{\sqrt{n}(c - \mu)}{\sigma} \right) \\ = \mathbb{P}_{\mu}\left( Z > \frac{\sqrt{n}(c - \mu)}{\sigma} \right) \\ = 1 - \Phi\left(\frac{\sqrt{n}(c - \mu)}{\sigma}\right). \ \ \ \ \ (9)")

) \\ = \underset{\mu \leq 0}{\text{sup}}\left(1 - \Phi\left(\frac{\sqrt{n}(c - \mu)}{\sigma}\right)\right) \\ = \beta(0) \\ = 1 - \Phi\left(\frac{c\sqrt{n}}{\sigma}\right). \ \ \ \ \ (10)")

. \ \ \ \ \ (11)")

}{\sqrt{n}}. \ \ \ \ \ (12)")

. For a test size of 95%

. For a test size of 95% ")

")

be \textsc{iid} random variables with

be \textsc{iid} random variables with }") . Let

. Let  be the estimate of

be the estimate of  be the standard deviation of the distribution of

be the standard deviation of the distribution of ")

. \ \ \ \ \ (16)")

where

where ")

) \\ = \underset{\theta \in \Theta_0}{\text{sup}}\mathbb{P}_{\theta}(X \in R) \\ = \mathbb{P}_{\theta_0}(X \in R) \\ = \mathbb{P}_{\theta_0}(|W| > z_{\alpha/2}) \\ = \mathbb{P}_{\theta_0}\left(\left| \frac{\hat { \theta } - \theta_0 }{\widehat{\textsf{se}}}\right| > z_{\alpha/2}\right) \\ \rightarrow \mathbb{P}(|Z| > z_{\alpha/2}) \\ = \alpha. \ \ \ \ \ (18)")

and

and  times, respectively, and have a probability of predicting with success as

times, respectively, and have a probability of predicting with success as  and

and  , respectively.

, respectively. .

.")

versus

versus  is

is  = \frac{ \underset{\theta \in \Theta_0}{\text{sup}} (L( \theta|\mathbf{x} )) }{ \underset{\theta \in \Theta}{\text{sup}} (L( \theta|\mathbf{x} )) }. \ \ \ \ \ (20)")

components:

components: }") . For

. For  ,

, moment as

moment as  = \mathbb{E}_\theta(X^j) = \int \mathrm{x}^{j}\,\mathrm{d}F_{\theta}(x). \ \ \ \ \ (1)")

")

is the value of

is the value of  = \hat{\alpha_1} \\ \alpha_2(\hat{\theta_n}) = \hat{\alpha_2} \\ \vdots \vdots \vdots \\ \alpha_k(\hat{\theta_n}) = \hat{\alpha_k} \ \ \ \ \ (3)")

}") . The likelihood function is defined as

. The likelihood function is defined as  = \prod_{i=1}^n f_X(X_i;\theta). \ \ \ \ \ (4)")

= \log(\mathcal{L}_n(\theta))}") .

. }") .

.}") distribution.

distribution.  = \begin{cases} 1/\theta 0 < x < \theta \\ 0 \text{otherwise}. \end{cases} \ \ \ \ \ (5)")

and

and  , then

, then  = 0}") . Otherwise

. Otherwise  = (\frac{1}{\theta})^n }") which is a decreasing function of

which is a decreasing function of \} = X_{max}}") .

.  and

and  are \textsc{pdf}, the Kullback Leibler distance between them is defined as

are \textsc{pdf}, the Kullback Leibler distance between them is defined as  = \int f(x) \log \left( \frac{f(x) }{g(x) } \right) dx. \ \ \ \ \ (6)")

}") . Then the score function is defined as

. Then the score function is defined as  = \frac{\partial \log f_X(x; \theta) }{\partial \theta}. \ \ \ \ \ (7)")

= \mathbb{V}_{\theta}\left( \sum_{i=1}^n s(X_i; \theta) \right) \\ = \sum_{i=1}^n \mathbb{V}_{\theta}\left(s(X_i; \theta) \right). \ \ \ \ \ (8)")

) = 0. \ \ \ \ \ (9)")

) = \mathbb{E}_{\theta}(s^2(X; \theta)). \ \ \ \ \ (10)")

= nI(\theta). \ \ \ \ \ (11)")

= -\mathbb{E}_{\theta}\left( \frac{\partial^2 \log f_X(x; \theta) }{\partial \theta^2} \right) \\ = -\int \left( \frac{\partial^2 \log f_X(x; \theta) }{\partial \theta^2} \right)f_X(x; \theta) dx. \ \ \ \ \ (12)")

} }") .

. }. \ \ \ \ \ (13)")

. \ \ \ \ \ (14)")

}} }") .

. . \ \ \ \ \ (15)")

}") traps

traps  . We call

. We call  is random and

is random and }") .

. be the \textsc{cdf} of a random variable

be the \textsc{cdf} of a random variable  with standard normal distribution and

with standard normal distribution and  \\ \mathbb{P}(Z > z _{\alpha / 2} ) = ( 1 - \alpha / 2) \\ \mathbb{P}(- z _{\alpha / 2} < Z < z _{\alpha / 2}) = 1 - \alpha. \ \ \ \ \ (16)")

\ \ \ \ \ (17)")

\rightarrow 1 - \alpha. \ \ \ \ \ (18)")

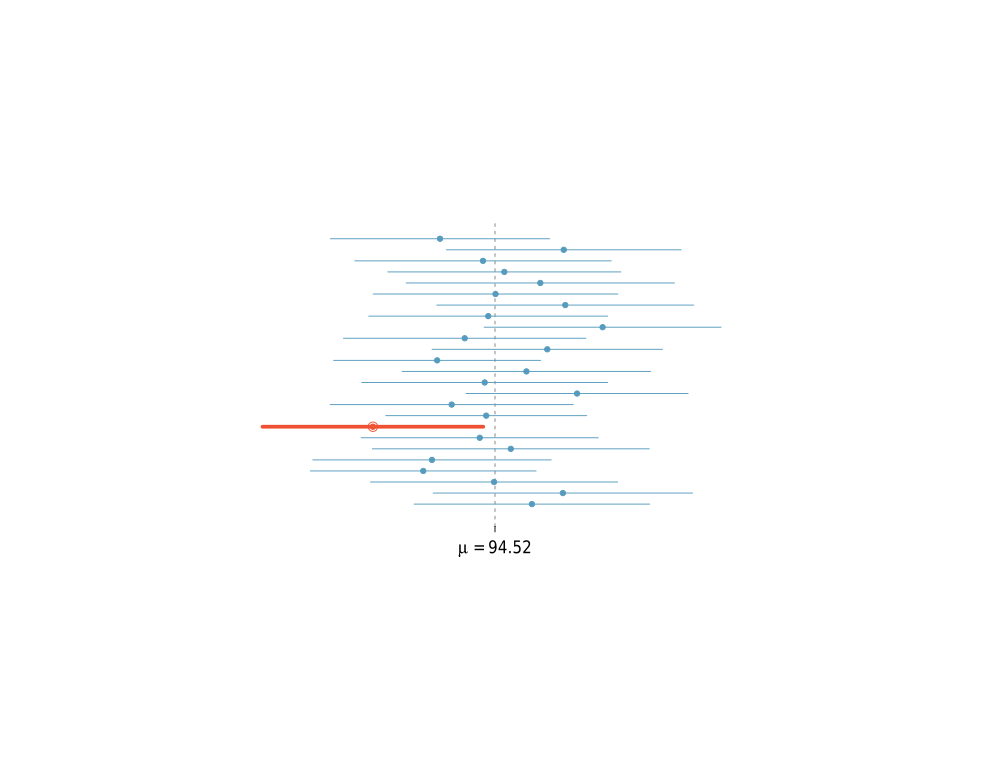

is .95,

is .95,  is 1.96 and the interval is thus

is 1.96 and the interval is thus  = \left( \hat{\theta} - 1.96\hat{\textsf{se}} , \hat{\theta} + 1.96\hat{\textsf{se}} \right) }") .

. : \theta \in \Theta\} \ \ \ \ \ (1)")

= \frac{1}{\sigma\sqrt{2\pi}}exp\{-\frac{1}{2\sigma^2}(x-\mu)^2\}, \mu \in \mathbb{R}, \sigma > 0\} \ \ \ \ \ (2)")

cannot be parameterized by a finite number of parameters.

cannot be parameterized by a finite number of parameters. is called a statistical functional.

is called a statistical functional.  is given as:

is given as:  = \int x dF(x) \ \ \ \ \ (3)")

= \int x^2 dF(x) - \left(\int xdF(x)\right)^2 \ \ \ \ \ (4)")

= F^{-1}(x) \ \ \ \ \ (5)")

,\dotsc,(X_n, Y_n)}") .

.  is assumed to depend on

is assumed to depend on  = \mathbb{E}(Y|X=x) \ \ \ \ \ (6)")

is finite dimensional, then the model is a parametric regression model, otherwise it is a non-parametric regression model.

is finite dimensional, then the model is a parametric regression model, otherwise it is a non-parametric regression model.  , then we call this regression or curve estimation.

, then we call this regression or curve estimation.  = \mathbb{E}(Y|X=x)}") can be algebraically manipulated to express it in the form

can be algebraically manipulated to express it in the form  + \epsilon \ \ \ \ \ (7)")

= 0}") .

. : \theta \in \Theta\}}") is a parametric model, then we write

is a parametric model, then we write  = \int_A f_X(x) dx }") to denote the probability that X belongs to A. It does not mean that we are averaging over

to denote the probability that X belongs to A. It does not mean that we are averaging over  . Since

. Since  : Formally, let

: Formally, let  of

of . \ \ \ \ \ (8)")

= \mathbb{E}( \hat{\theta} ) - \theta. \ \ \ \ \ (9)")

.

.  = \sqrt{\mathbb{V}(\hat{\theta})}. \ \ \ \ \ (10)")

= \mathbb{E}_{ \theta } ( \hat{\theta} - \theta)^2. \ \ \ \ \ (11)")

. Then,

. Then,  = p}") . Hence,

. Hence,  is unbiased.

is unbiased. . \ \ \ \ \ (12)")

}") (where

(where  }") and

and  }") are functions of the data), such that

are functions of the data), such that  \geq 1 - \alpha, \forall \: \theta \in \Theta. \ \ \ \ \ (13)")

\\ \mathbb{P}(Z > z _{\alpha / 2} ) = ( 1 - \alpha / 2) \\ \mathbb{P}(- z _{\alpha / 2} < Z < z _{\alpha / 2}) = 1 - \alpha. \ \ \ \ \ (14)")

\ \ \ \ \ (15)")

\rightarrow 1 - \alpha. \ \ \ \ \ (16)")

converges in probability to the distribution mean

converges in probability to the distribution mean  and let

and let  converges to

converges to  , if for every

, if for every  , we have

, we have  \rightarrow 0 \ \ \ \ \ (1)")

.

. , if

, if  = F(t) \ \ \ \ \ (2)")

for which

for which  be \textsc{iid} with mean

be \textsc{iid} with mean }") and variance

and variance }") . Let sample mean be defined as

. Let sample mean be defined as \sum_{i=1}^n X_i}") . It can be shown that

. It can be shown that  = \mu}") and

and  = \sigma^2/n}") .

. .

.  } { \sqrt{ \mathbb{V}( \overline{X}_n ) } } = \frac{ \sqrt{n}(\overline{X}_n - \mu) } { \sigma } \rightsquigarrow N(0,1) \ \ \ \ \ (3)")

\\ \overline{X}_n \approx N\left(\mu, \frac{\sigma^2}{n}\right) \\ (\overline{X}_n - \mu) \approx N(0, \sigma^2/n) \\ \sqrt{n}(\overline{X}_n - \mu) \approx N(0,\sigma^2) \\ \frac{\sqrt{n}(\overline{X}_n - \mu)}{\sigma} \approx N(0,1). \ \ \ \ \ (4)")

^2\right). \ \ \ \ \ (5)")

}{S_n} \approx N(0,1). \ \ \ \ \ (6)")

be a random variable with conditions of CLT met, and let

be a random variable with conditions of CLT met, and let }") be a differentiable function with

be a differentiable function with  \neq 0}") . Then,

. Then,  \\ \Longrightarrow \quad g(Y_n) \approx N\left(g(\mu), (g'(\mu))^2\frac{\sigma^2}{n}\right). \ \ \ \ \ (7)")

= \int x f(x) dx = \begin{cases} \sum_x x f(x) X \text{ is discrete} \\ \int_x x f(x) dx X \text{ is continuous}. \end{cases} \ \ \ \ \ (1)")

= \mathbb{E}X = \int x \thinspace dF(x) = \mu_X = \mu \ \ \ \ \ (2)")

}") , then the expectation of Y is

, then the expectation of Y is  = \int r(X) \thinspace dF_X(x). \ \ \ \ \ (3)")

are constants, then

are constants, then  = \sum_{i=1}^na_i\mathbb{E}(X_i). \ \ \ \ \ (4)")

= \prod_{i=1}^n\mathbb{E}(X_i). \ \ \ \ \ (5)")

}") ,

,  , or

, or  is defined by:

is defined by:  = \mathbb{E}((X - \mu)^2) = \int (X - \mu)^2 \thinspace dF(x) \ \ \ \ \ (6)")

. \ \ \ \ \ (7)")

^2\right). \ \ \ \ \ (8)")

= \mathbb{E}(X^2) - \mu^2. \ \ \ \ \ (9)")

and

and  = a^2 \mathbb{V}(X). \ \ \ \ \ (10)")

= \sum_{i=1}^n{a_i}^2\mathbb{V}(X_i). \ \ \ \ \ (11)")

= \mu, \quad \mathbb{V}(\overline{X}_n) = \frac{\sigma^2}{n} \quad \text{ and } \quad \mathbb{E}(S_n^2) = \sigma^2. \ \ \ \ \ (12)")

")

}") to outcomes

to outcomes  in

in  .

. ![{F_X \colon \mathbb{R} \rightarrow [0,1]}](http://s0.wp.com/latex.php?latex=%7BF_X+%5Ccolon+%5Cmathbb%7BR%7D+%5Crightarrow+%5B0%2C1%5D%7D&bg=ffffff&fg=000000&s=0 "{F_X \colon \mathbb{R} \rightarrow [0,1]}") defined by:

defined by:

= \mathbb{P}(X \leq x) \ \ \ \ \ (2)")

. If

. If  = G(x)}") for all

for all  then

then  = \mathbb{P}(Y \in A)}") for all

for all  .

.  = \mathbb{P}(X = x)}") .

.  such that

such that  \geq 0}") for all

for all dx = 1}")

with

with  we have

we have

dx = \mathbb{P}(a < X < b) \ \ \ \ \ (3)")

= \int_{-\infty}^x f_X(t)dt \ \ \ \ \ (4)")

= F_X'(X)}") at all points for which

at all points for which  is differentiable.

is differentiable.  to denote that the random variable

to denote that the random variable  if

if  = 1}") . Hence

. Hence  = \begin{cases} 0& x < a \\ 1& x \geq a. \end{cases} \ \ \ \ \ (5)")

be a given integer. Let

be a given integer. Let  = \begin{cases} 1/k & 1 \leq x \leq k \\ 0 & \text{otherwise}. \end{cases} \ \ \ \ \ (6)")

.

. = p}") and

and  = 1 - p}") for some

for some ![{p \in [0, 1]}](http://s0.wp.com/latex.php?latex=%7Bp+%5Cin+%5B0%2C+1%5D%7D&bg=ffffff&fg=000000&s=0 "{p \in [0, 1]}") . We say that

. We say that }") . The probability function

. The probability function  = p^x(1 - p)^{(1 - x)} \text{ for } x \in {0, 1}}") .

. denotes the probability of getting heads in a single coin toss and the tosses are assumed to be independent then the \textsc{pdf} of

denotes the probability of getting heads in a single coin toss and the tosses are assumed to be independent then the \textsc{pdf} of  = \begin{cases} \begin{pmatrix} n \\ x \end{pmatrix} p^x(1 - p)^{(n-x)} & 0 \leq x \leq n \\ 0 & \text{otherwise}. \end{cases} \ \ \ \ \ (7)")

}") if

if  = p(1 - p)^{(x - 1)} \text{ for } x \in \{1, 2, 3, \dotsc , \}. \ \ \ \ \ (8)")

, written as

, written as }") if

if  = e^{-\lambda}\frac{\lambda^{-x}}{x!} \text{ for } x \geq 0. \ \ \ \ \ (9)")

, X has a uniform distribution over

, X has a uniform distribution over }") , if

, if ![\displaystyle f_X(x) = \begin{cases} \frac{1}{b - a} & x \in [a, b] \\ 0 & \text{otherwise}. \end{cases} \ \ \ \ \ (10)](http://s0.wp.com/latex.php?latex=%5Cdisplaystyle++f_X%28x%29+%3D+%5Cbegin%7Bcases%7D+%5Cfrac%7B1%7D%7Bb+-+a%7D+%26+x+%5Cin+%5Ba%2C+b%5D+%5C%5C+0+%26+%5Ctext%7Botherwise%7D.+%5Cend%7Bcases%7D+%5C+%5C+%5C+%5C+%5C+%2810%29&bg=ffffff&fg=000000&s=0 "\displaystyle f_X(x) = \begin{cases} \frac{1}{b - a} & x \in [a, b] \\ 0 & \text{otherwise}. \end{cases} \ \ \ \ \ (10)")

}") if

if  = \frac{1}{\sigma\sqrt{2\pi}}exp\left\{-\frac{1}{2\sigma^2}(x-\mu)^2\right\}, \text{ where } \mu, \sigma \in \mathbb{R}, \sigma > 0. \ \ \ \ \ (11)")

and

and  . A standard Normal random variable is denoted by

. A standard Normal random variable is denoted by }") and

and }") . The \textsc{pdf} is plotted in Figure There is no closed-form expression for

. The \textsc{pdf} is plotted in Figure There is no closed-form expression for  / \sigma \sim N(0, 1)}") .

.

}") , then

, then }") .

.

}") for

for  are independent, then we have

are independent, then we have

. \ \ \ \ \ (12)")

}") that if

that if  \ \ \ \ \ (13)")

= \mathbb{P}\left(a < \mu + \sigma Z < b\right) \ \ \ \ \ (14)")

= \mathbb{P}\left(\frac{a - \mu}{\sigma} < Z < \frac{b - \mu}{\sigma}\right) \ \ \ \ \ (15)")

= \Phi\left(\frac{b - \mu}{\sigma}\right) - \Phi\left(\frac{a - \mu}{\sigma}\right). \ \ \ \ \ (16)")

}") . Find

. Find }") .

. \\ = \mathbb{P}\left(3 + Z\sqrt{5} > 1\right) \\ = \mathbb{P}\left( Z > \frac{-2}{\sqrt{5}}\right) \\ = 1 - \Phi\left(\frac{2}{\sqrt{5}}\right) \\ = 1 - \Phi\left(0.894427\right) \\ = 0.81. \ \ \ \ \ (17)")

of

of  = .2}") . Solution:

. Solution:  \\ = \mathbb{P}\left(3 + Z\sqrt{5} < x\right) \\ = \mathbb{P}\left(Z < \frac{x - 3}{\sqrt{5}}\right) \\ = \Phi\left(\frac{x - 3}{\sqrt{5}}\right) \ \ \ \ \ (18)")

= 0.2}")

= \Phi\left(\frac{x - 3}{\sqrt{5}}\right) \\ -0.8416 = \left(\frac{x - 3}{\sqrt{5}}\right) \\ x = \left(3 - 0.8416\times\sqrt{5}\right) \\ x = 1.1181. \ \ \ \ \ (19)")

, written as

, written as }") , if

, if  = \frac{1}{\beta}e^{-x/\beta}, \text{ for } x > 0. \ \ \ \ \ (20)")

, the Gamma function is defined as

, the Gamma function is defined as  = \int_0^\infty y^{\alpha - 1} e^{-y} dy. \ \ \ \ \ (21)")

), written as

), written as }") , if

, if  = \frac{1}{\beta^{\alpha}\Gamma(\alpha)}x^{\alpha - 1}e^{-x/\beta}, \text{ for } x > 0. \ \ \ \ \ (22)")

= \mathbb{P}(X = x, Y = y)}")

a \textsc{pdf} of random variables

a \textsc{pdf} of random variables }") if

if  \geq 0}") for all

for all  \in \mathbb{R}^2}") ,

,

\thinspace dx \thinspace dy = 1}")

we have

we have

\thinspace dx \thinspace dy = \mathbb{P}((X,Y) \in A). \ \ \ \ \ (23)")

, let

, let  = \begin{cases} cx^2y x^2 \leq y \leq 1, \\ 0 \text{otherwise}. \end{cases} \ \ \ \ \ (24)")

.

. to

to  and find

and find  \thinspace dy \thinspace dx \\ = \int_{-1}^{1}\int_{x^2}^{1}f_{X,Y}(x, y) \thinspace dy \thinspace dx \\ = \int_{-1}^{1}\int_{x^2}^{1}cyx^2 \thinspace dy \thinspace dx \\ = \int_{-1}^{1}c\left(\frac{1 - x^4}{2}\right)x^2 \thinspace dx \\ = \left(\frac{c}{2}\right)\left(\int_{-1}^{1}x^2 \thinspace dx - \int_{-1}^{1}x^6 \thinspace dx \right)\\ = \left(\frac{c}{2}\right)\left( \frac{2}{3} - \frac{2}{7}\right)\\ = \left(\frac{4c}{21}\right) \\ c = \frac{21}{4} \ \ \ \ \ (25)")

have a joint mass distribution

have a joint mass distribution  then the marginal distribution of

then the marginal distribution of  = \mathbb{P}(X = x) = \sum_y \mathbb{P}(X = x, Y = y) = \sum_y f_{X,Y}(x, y) \ \ \ \ \ (26)")

= \mathbb{P}(Y = y) = \sum_x \mathbb{P}(X = x, Y = y) = \sum_x f_{X,Y}(x, y) \ \ \ \ \ (27)")

= \int f_{X,Y}(x, y) \thinspace dy \ \ \ \ \ (28)")

= \int f_{X,Y}(x, y) \thinspace dx \ \ \ \ \ (29)")

we have

we have  = \mathbb{P}(X \in A)\mathbb{P}(Y \in B) \ \ \ \ \ (30)")

if

if  = f_X(x)f_Y(y)}") for all values of

for all values of  = \frac{f_{X, Y}(x, y)}{f_Y(y)} \ \ \ \ \ (31)")

where

where }") denote their \textsc{pdf}. We say that

denote their \textsc{pdf}. We say that  ,

,  = \prod_{i=1}^n \mathbb{P}(X_i \in A_i) \ \ \ \ \ (32)")

")

. We also call

. We also call ")

}") are independent. The joint density of

are independent. The joint density of  = \frac{1}{{(2\pi)}^{k/2}}\text{exp}\biggl\{-\frac{1}{2}\sum_{j=1}^k {z_j}^2\biggr\} = \frac{1}{{(2\pi)}^{k/2}}\text{exp}\left\{-\frac{1}{2}z^Tz\right\} \\ f_X(x;\mu, \Sigma) = \frac{1}{{(2\pi)}^{k/2}{|\Sigma |}^{1/2}}\text{exp}\left\{-\frac{1}{2}(x - \mu)^T\Sigma^{-1}(x - \mu)\right\} \ \ \ \ \ (35)")

and the event that the first toss is heads is

and the event that the first toss is heads is  .

.  is the false event.

is the false event.  are mutually exclusive events if

are mutually exclusive events if  whenever

whenever  .

.  is called a probability measure or a probability distribution if it satisfies the following three axioms:

is called a probability measure or a probability distribution if it satisfies the following three axioms:

= 1}") .

.

\geq 0}") for every

for every  are disjoint, then:

are disjoint, then:

= \sum_{i=1}^{\infty}\mathbb{P}(A_i) \ \ \ \ \ (2)")

= 0 \ \ \ \ \ (3)")

\leq \mathbb{P}(B) \ \ \ \ \ (4)")

\leq 1 \ \ \ \ \ (5)")

= 1 - \mathbb{P}(A) \ \ \ \ \ (6)")

= \mathbb{P}(A) + \mathbb{P}(B) \ \ \ \ \ (7)")

= \mathbb{P}(A) + \mathbb{P}(B) - \mathbb{P}\left(A \bigcap B\right) \ \ \ \ \ (8)")

, then

, then  \rightarrow \mathbb{P}(A) \ \ \ \ \ (9)")

is finite and each outcome is equally likely, then:

is finite and each outcome is equally likely, then:  = \frac{|A|}{|\Omega|} \ \ \ \ \ (10)")

\times n \ \ \ \ \ (11)")

}") out of them is

out of them is !} \ \ \ \ \ (12)")

!} = \frac{20 \times 19 \times 18}{1 \times 2 \times 3} = 1140 \ \ \ \ \ (13)")

= \mathbb{P}(A)\mathbb{P}(B) \ \ \ \ \ (14)")

is independent if

is independent if  = \prod_{i \in J} \left(\mathbb{P}(A_i)\right) \ \ \ \ \ (15)")

of

of  .

.  = \frac{\mathbb{P}(A \bigcap B)}{\mathbb{P}(B)}. \ \ \ \ \ (16)")

}") is the fraction of times

is the fraction of times  = \mathbb{P}(A)}") . Also, for any pair of events

. Also, for any pair of events  = \mathbb{P}(A|B)\mathbb{P}(B) = \mathbb{P}(B|A)\mathbb{P}(A). \ \ \ \ \ (17)")

be a partition of

be a partition of  = \sum_{i=1}^n \mathbb{P}(B|A_i)\mathbb{P}(A_i). \ \ \ \ \ (18)")

> 0 }") for each

for each  . If

. If  > 0}") , then for each

, then for each  :

:

= \frac{\mathbb{P}(B|A_i)\mathbb{P}(A_i)}{\sum_{j=1}^n \mathbb{P}(B|A_j)\mathbb{P}(A_j)}. \ \ \ \ \ (19)")

: The probability of the partition events given the single event

: The probability of the partition events given the single event  : The probability of the single event

: The probability of the single event  are the events that an email is spam, low priority or high priority, respectively. Let

are the events that an email is spam, low priority or high priority, respectively. Let  = .7, \thinspace \mathbb{P}(A_2) = .2, \text{ and } \mathbb{P}(A_3) = .1 }") .

.  = .9, \thinspace \mathbb{P}(B|A_2) = .02, \text{ and } \mathbb{P}(B|A_3) = .01 }") .

.  = \mathbb{P}(A_1|B) \ \ \ \ \ (20)")

= \frac{\mathbb{P}(B|A_1)\mathbb{P}(A_1)}{\sum_{j=1}^3 \mathbb{P}(B|A_j)\mathbb{P}(A_j)} = \frac{.9 \times .7}{.9 \times .7 + .01 \times .2 + .01 \times .1} = .995. \ \ \ \ \ (21)")